In Europe, Sales of Plant-Based Meat & Dairy Grew by 6% – But Price Parity Holds the Key

5 Mins Read

Despite the industry’s headwinds, retail sales of plant-based food in six major European markets increased by 5.5%, and lower prices can help bring a windfall for companies in this space.

There have been a few too many doomsday-like headlines about the plant-based world in recent months, adding to a divisive narrative that the industry’s best days were behind it.

The reality is, in the US, all but four categories in the vegan sector saw sales plummet last year. And in Europe, retail sales of meat and dairy analogues collectively increased in 2023 compared to the previous year.

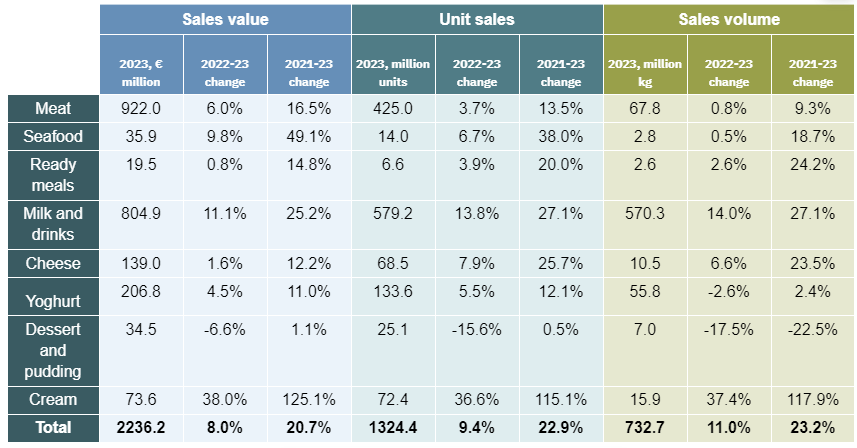

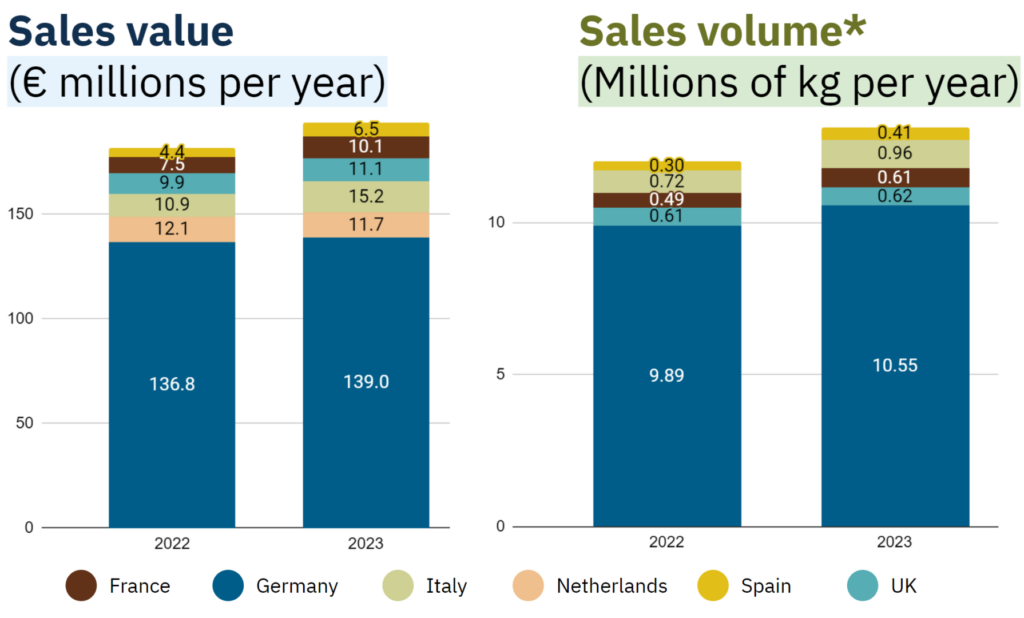

This is according to analysis of previously unpublished Circana data by the Good Food Institute (GFI) Europe, which found that in the six largest European economies – Germany, the UK, France, Italy, Spain, and the Netherlands – the sales value of plant-based food rose by 5.5% in 2023, reaching €5.4B. At the same time, the volume of sales measured by weight also grew by 3.5%.

“Europe’s plant-based sector has continued to make headway despite a difficult few years for the wider food industry,” said Helen Breewood, research and resource manager at GFI Europe.

“Plant-based meat and dairy are becoming mainstream options in many European countries, emerging plant-based categories are growing, and some products are beginning to compete with their animal-based counterparts on price.”

Here are our five major takeaways from GFI Europe’s analysis of vegan food sales in Europe.

Alt-milk remains king

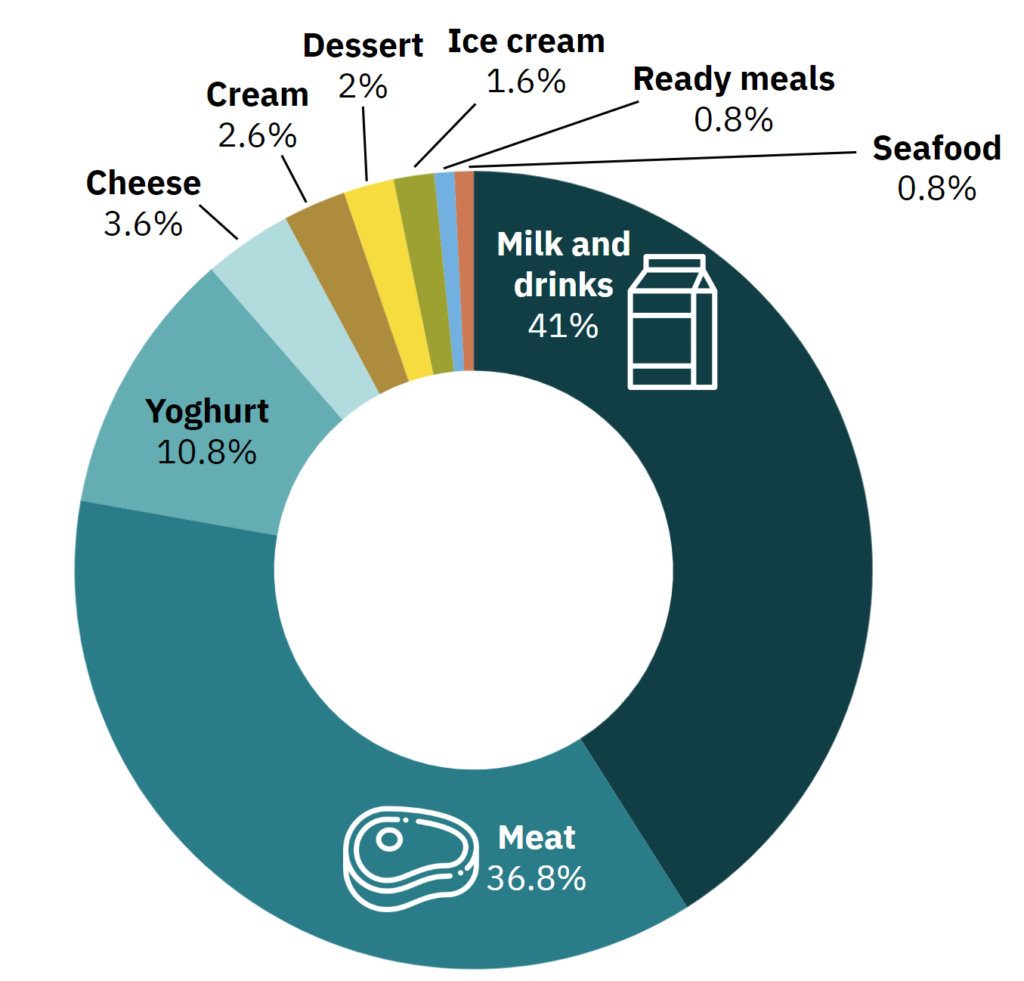

Like the rest of the world, plant-based milk has remained the largest category in Europe, accounting for 41% of all sales in 2023. This was facilitated by a 7% hike in sales value, reaching €2.2B. Unit sales also grew by 4.7%, and product volumes were up by 5.2%.

Germany is the largest plant-based milk market, netting €805M in sales value (a 37% share). This is explained by the shrinking price gap between milk alternatives and conventional dairy, which was down from 35% in 2021 to just 3% in 2023. If the VAT on the former (19%) was the same as the latter (7%), price parity would have already been achieved.

Meat analogues are second on the list with a 37% share of Europe’s vegan sales. Between 2022 and 2023, the sales value of these products was up by 3.2%, reaching €2B, while units were steady and volumes declined.

Germany retains top spot for plant-based

The land of bratwurst was already the largest in Europe, and it continued to dominate, taking up 40% of the market (€2.2B) among the countries analysed.

Despite being the most profitable nation for plant-based milk producers, Germany bucks the continental trend by selling more meat analogues than alt-dairy. This is because it is also the largest market for meat-free products, accounting for nearly half (46%) of all sales.

The number of households these products are reaching is also rising steadily, if gradually – plant-based meat penetrated 37.4% of households last year (versus 33.8% in 2021), and milk alternatives were bought by 36.5% (up from 36.3% two years prior).

The UK is next on the list in terms of market size, with sales reaching €942M. It was followed by France (€648M), Italy (€641M), Netherlands (€452M) and Spain (€309M).

Where sales declined, the slump may be over

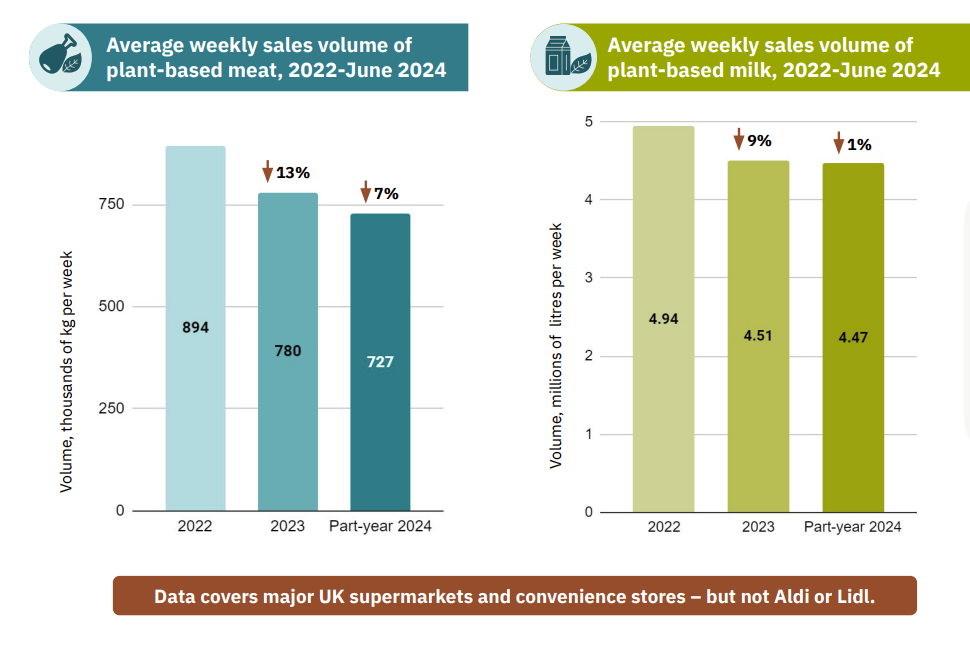

In only two markets did plant-based products perform worse in 2023 than the year before: the UK and the Netherlands. The former saw sales decline by 2.8% (with a larger 10% drop in volume), while in the latter, volume sales were down by 5%, with units dipping by 1%.

However, there are signs that this slowdown started to level off in 2023 and the early months of this year. For starters, the sales value of plant-based products in the Netherlands actually grew by 1%, and volumes have shown a slight rebound after two years of decline.

In the UK, weekly unit sales of meat analogues fell by 7% in early 2024, compared to a 12% decrease last year. And plant-based milk experienced a 1% decline in unit sales per week this year, versus 9% in 2023. And just this week, discount retailer Lidl announced it is tripling its own-label plant-based offering after seeing demand grow by 12% last year.

Europeans love non-dairy cheese and cream

Two categories that shone last year were cream and cheese alternatives. Vegan cheese, taking up 3.6% of the total share, was the fastest-growing product in Spain, France and Italy, and plant-based cream (comprising 2.6% of the market) experienced the quickest growth in Germany, the Netherlands, and the UK.

The latter made 24% more money in 2023, representing the highest sales hike of any category, albeit being a much smaller category than vegan milk, meat, and yoghurt.

On the other hand, plant-based desserts (-3%), non-dairy ice cream (-8%), and vegan ready meals (-10% in France, Germany and the UK) have witnessed drop-offs, which GFI Europe ascribed to cost-of-living pressures that led shoppers to cut back on non-essential and convenience items.

Price parity is priceless

A major finding of the analysis was that with certain products and in certain markets, the price gap between animal proteins and their vegan versions has closed – and this has been associated with better sales.

For example, branded dairy-free creams are cheaper than their conventional counterparts in Germany and the UK, spurring a 23% sales hike in the latter. In fact, private-label plant-based milk costs an average of €1.12 per litre, 13% cheaper than own-label dairy milk (€1.30).

Likewise, higher prices mean middling sales. With volume sales of plant-based meat down, manufacturers need to develop products that meet consumer expectations on both taste and price.

So finding ways to lower prices is key to the success of plant-based meat and dairy in Europe. “Our analysis finds that lower prices and higher quality can power the growth of these more sustainable options, so policymakers and manufacturers should continue to invest in innovation and infrastructure to develop tastier, more affordable products capable of building a diversified, resilient and healthy European food system,” said Breewood.

Author