Opinion: Future Food Tech Funding Needs A Complete Overhaul

12 Mins Read

Funding future food innovations is crucial. As traditional VCs look elsewhere, it’s for the sector to welcome new and diverse sources of investment, from blended capital to redeemable equity.

By Sonalie Figueiras, founding editor at Green Queen Media and advisor at Better Bite Ventures, Mudcake and Alwyn Capital, and Maximilian von Poelnitz, Venture Partner at Ajinomoto Corporate Venture Capital

Over the past five years, we have seen a food tech hype bubble building as generalist investors entered the space in droves attracted by the promise of backing climate solutions, the realization that the current food system faces existential challenges, hundreds of passionate mission-led founders, a handful of IPOs that made global headlines because of outsized returns, social media-fueled foodie trends and the promise of helping make the world a better, more environmentally-friendly place. More simply put, food innovation became sexy.

Over time, a disconnect formed between R&D initiatives and go-to-market strategies, and while new money flooded the space, deep sector expertise and long-term track records were hard to come by.

This culminated in the easy money and public stock market euphoria of 2020 and 2021 especially with Covid-led government cash infusions. By 2023, the bubble had burst, and over the past 12 months food tech companies have seen their valuations slashed, dozens of startups have disappeared from the space and the generalist money has moved on to new pastures like climate tech, with funding rounds drying up.

The pendulum has now swung back in favour of cash-infused investors and companies that are actively prolonging runway and driving a clear path to commercialization and profitability. This is problematic for deep tech companies in sectors like cellular agriculture and precision fermentation where there is still a lot of work to do to drive bench-scale applications to industrial and commercial scale distribution; many companies will struggle to move from the lab to the open market without access to capital.

Foodtech investing today: burned by hype

So what went wrong? Ultimately, investors were led to believe that food tech could behave like a tech business and that distribution was simple. There was a sense of ‘build it and they will come’. In 2019/2020, CAGR calculations also made for easy math given that alternative protein markets were growing at over 15% annualized and in some sectors like dairy at over 50%. This led to further media hype and many new /generalist investors jumping into the sector feet-first. Ultimately both the production and distribution math was challenged as startups continue to struggle to move from pilot scale to commercial scale. Further demand for innovative products driven by taste and texture will contribute to additional adoption but not based on the timelines that investors were originally sold.

Foodtech as an investment class: one brush cannot apply to all types

One of the most important “resets” to have occurred over the past 12 months has been investors recognizing that food businesses are not SAAS or technology companies. The term food tech really should not be seen as a catch-all but rather spans a wide variety of industries that include biotech, CPG and/or ingredient-focused R&D houses. This ultimately requires investors with deep expertise in each and a much more niche focus, and in certain verticals, a far longer time horizon for exit.

Except for a few innovation-led plant-based companies like Impossible Foods (precision fermentation-derived heme), Climax Foods (plant casein IP), or EQUII (protein-enriched flour), most plant-based food/meat companies are CPG plays and should be classified (and diligenced) as such. A CPG venture capital firm ultimately has a different investment thesis than a deep-tech fund.

While there is a long history of successful investments and M&A in the food space, the reality is that a Danone will never be a Google or an Apple in terms of market share and revenues – the food business simply does not have the same unit economics as software companies.

Investor Daniel Gluck wrote about these differences in a social media post: “CPG companies don’t scale as fast as tech, typically. Like tech, CPG focuses on creating and changing habits. But customers are more adventurous with apps on their phone than food on their shelves. Most retailers take on new products only 1 to 2 times a year. Customer adoption takes time and growth is slow.”

Wired journalist Matt Reynolds reports further: “Food isn’t like the technology industry, Reams points out. Food companies—even ones with a cool technological edge—do not grow like a software company, he says. Food companies operate on razor-thin margins, prices are volatile, and customers can be extremely picky about what they’ll put in their mouths. There’s also a scaling issue. Software companies can scale rapidly because getting their product to new customers costs almost nothing. It’s just a matter of duplicating lines of code, or hooking up a user to a centralized database that already exists. Food isn’t like that. Every extra plant-based burger requires more soy and pea plants that have to be grown, plus labor costs and processing time. Bigger factories and more efficient production will reduce the cost per burger, but scaling is a slow process that requires expensive physical infrastructure, with no guarantee that customers will buy those slightly-cheaper burgers once they’re made.”

That being said, liquidity events exist every year as large incumbents such as General Mills, PepsiCo, Netsle, or Unilever continue to be active in the space. The takeaway here is that this makes for a completely different investor base as and life cycle.

Food is not ‘frivolous’

With the challenges facing the industry, there continues to be an existential need for food tech solutions and productivity gains. The recent hype cycles in the industry and the failures that continue to gain media attention do not change the fact that the industry is solving a core problem: the very real issues facing our global food systems, which are responsible for a third of global greenhouse gas (GHG) emissions. We cannot solve the climate crisis without evolving our food systems.

In a piece asking whether the venture capital model is broken, James Ledbetter writes of the sector’s frivolity problem: “Venture capital’s frivolity or lemming problem is not recently acquired. The Internet highway is littered with roadkill of venture-backed companies that would have been considered silly even if they had succeeded.” As we consider how the food industry can benefit from different funding structures and formats, it’s important to state that food, unlike many flash-in-the-pan apps, is anything but frivolous. Food is an essential part of human daily life and must be accorded the importance it merits.

Deeptech food: a longer game

Over the past five years, the term food tech has also come to mean a key focus on synthetic biology, precision fermentation, and even cellular agriculture. These represent sectors with very different capital requirements and investment horizons compared to a standard plant-based meat alternative product.

Deep-tech and cultivated meat/food tech companies have more parallels with healthcare technology given their long R&D cycles, some form of regulatory approval, and the need to plan distribution and supply chain effectively. More importantly, these businesses come with significant infrastructure needs whether through co-manufacturing agreements or a self-designed manufacturing hub. At each business milestone, the company or start-up requires different forms of capital that cannot be supported purely by the venture capital industry.

The key concern in the functional food tech industry is innovators moving from bench scale to pilot scale and then ultimately to commercial scale. Each stage requires a significant investment and technically the risk profile is reduced at each stage. In 2023, venture capital investors tend to shy away from deals where 50% of the capital is put into capex. Again, there are clear parallels with the traditional healthcare biotech inverter landscape. At pilot scale, food tech companies need access to other forms of capital as they begin to take what they created in a lab and bring it to market.

Ultimately, the industry is at a tipping point as it awaits better infrastructure, more project finance, and greater government support. Infrastructure projects do not lend to venture capital timelines. For investors, the next few years will involve increased consolidation and survival exercises by several larger startups. This will potentially be very good for a few early movers but still requires these businesses to find product market fit and commercial success.

Foodtech (esp deep-tech sectors like cultivated meat) has an investment horizon problem: VC exit timelines don’t match technology lifecycles. In the healthcare space, there is a mechanism for VCs to exit their investments as a new round of investors might join at the clinical trial stage. Ultimately food tech needs a milestone-driven approach that allows for other forms of patient capital to enter the investment pool.

So where do we go from here?

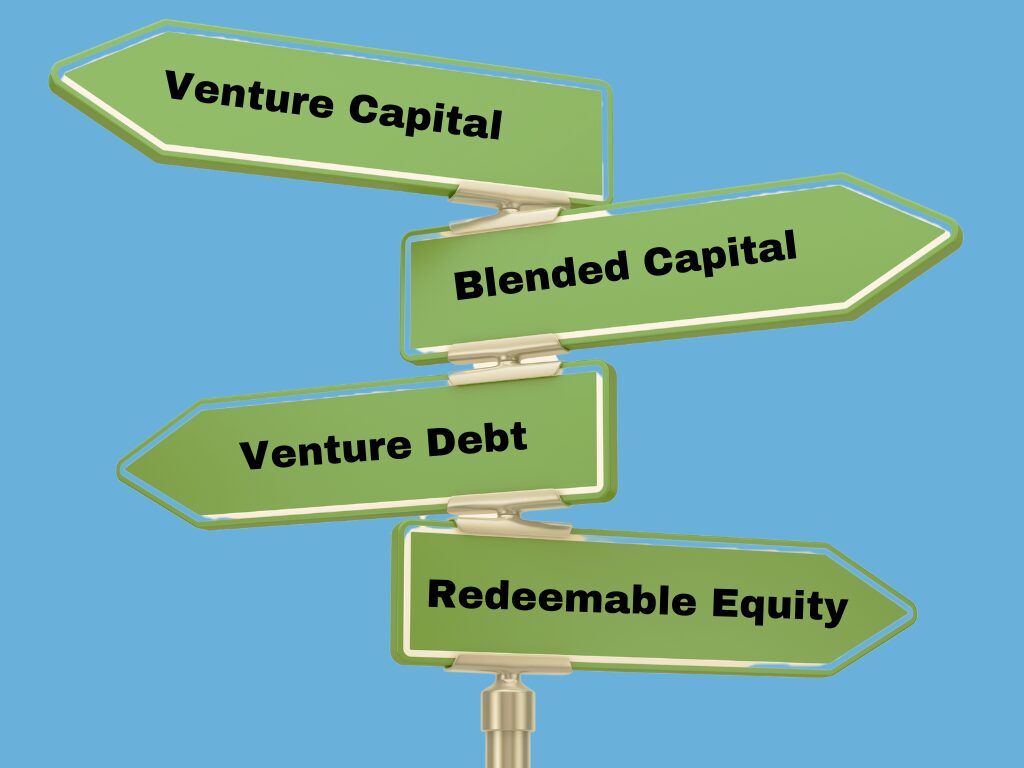

What’s clear is that the classic Silicon Valley VC model is not necessarily adapted to the needs of systemic food system change. To finance a transition to a less carbon-intensive, more resilient global food system that meets the needs of humanity ethically, sustainably and nutritionally, new types of capital are needed. Below we explore some of the possibilities.

Patient capital

Patient capital does not have a rigid definition, but generally, the term refers to long-term investments where investors are prepared to wait a considerable amount of time (3-5 years in some sectors, 10-15 years in others) before seeing any financial returns. For this reason, fund managers implementing a patient capital strategy will maintain their investments even if they’re seeing short-term losses for the fund. Pension funds and sovereign wealth funds are typical examples of patient capital. In recent years, patient capital has also come to be associated with impact investing. In this context, rather than maximising immediate returns for shareholders, the focus is on maximising the positive social or environmental impact of an investment, alongside financial gains. Non-profit investment fund Acumen, for instance, defines patient capital as “investment in an early-stage enterprise providing low-income consumers with access to healthcare, water, housing, alternative energy, or agricultural inputs.”

Both patient capital and venture capital seek a return on investment. Besides its longer time horizon, however, patient capital also has a higher risk tolerance than traditional forms of investment and can perhaps provide more follow-on investment in the event that a company enters a challenging capital environment.

Blended/public capital

Food is a commonwealth sector- we all need a better food system. Investing in food system solutions should involve commonwealth interests, including taxpayer money, and should be based on defined criteria around finding solutions to the biggest problems of our time such as bulwarking our global food system against the consequences of climate change.

We need more blended capital solutions, where public funds match private sector investment, effectively doubling funding rounds for young startups. Given food’s importance in society, governments should be actively participating in the future food sector and investing in innovation and talent. A great example of the successful deployment of blended/public capital is the Bpifrance story (Banque Publique d’Investissements France), the French government’s investment bank arm.

In an in-depth piece for Sifted, reporter Chris O’Brien writes about the success of ‘La French Tech’ being underwritten by Bpifrance:

“To understand the secret of France’s entrepreneurial boom, take a close look at state bank Bpifrance, an economic beast whose tentacles reach into every corner of this nation’s innovation ecosystem. Between direct and indirect investments, Bpifrance poured €1.6bn into French tech startups and venture funds in 2022 alone, up from €1.51bn in 2021…A closer look at the cap tables of the 120 companies reveals that 51 raised some kind of direct investment from Bpifrance, according to Dealroom…Even in Europe, where government investment in the economy is de rigueur, Bpifrance stands apart. And, a decade after its creation, its mission continues to expand with programmes to stop climate change and rebuild France’s industrial base.”

The ‘Shared Prosperity’ model and redeemable equity

Gutter Capital offers a model they dub “shared prosperity”, a model that “derives from 16th century maritime commerce…“Sailing crude vessels on treacherous routes from Europe to Asia and the Americas, early navigators risked death or capture on the high seas to deliver their cargo. As compensation, ship captains would take 20% of the profit from goods carried. Carried interest was born. Today, carried interest refers to how venture capitalists are compensated, taking 20% of the profits from the investments they make. Where sea captains risked life and limb to earn their keep, today’s venture capitalists enjoy the spoils of conquest while remaining safe on shore…The Gutter Infinity Fund will attempt to share the wealth by spreading both risks and rewards across the fund’s stakeholders…Our view is that founders are getting a raw deal,” Teran tells Fast Company, “so we’re putting our money where our mouth is and doing something about it.”

Food tech companies can also consider nontraditional equity structures such as redeemable equity. Can Atacik, founder of Alethina Impact Investments and Advisory, founding partner of ImpACTNOW Capital, and a venture partner of Venture Science talks about how climate entrepreneurs in particular can leverage redeemable equity to raise funding on alternative terms.

“Some climate founders may have a venture that doesn’t have a likely exit on a 10-15 year horizon (or exiting may not even be the right outcome). Keeping the business private long-term may lead to better business outcomes and climate impact, and founders may want to have the right to regain ownership over time.”

Redeemable equity enables founders to buy back ownership from VCs at pre-defined terms, which means investors can still have a compelling exit without forcing an IPO or acquisition. While the upside can be lower, a redeemable structure does mean greater downside protection than traditional VC.

An increasing (though small) number of startups are pursuing non-traditional equity models during fundraising. A German femtech team just raised a seed round that included the co-founder creating her own sustainable financing instrument, dubbed the Future Profit Partnership Agreement (FPPA). As reported here, she developed a “a mezzanine financial instrument that combines advantages of equity and debt capital and enables an appropriate return for investors…Instead of a conventional equity round, they offer a profit share. The agreement ends as soon as the return is achieved…Profits are a means to an end and are reinvested, used to cover capital costs or donated.”

Venture debt

With the collapse of Silicon Valley Bank (SVB), there has been a significant uptake in financial services and banks targeting venture debt (the higher interest rate environment has helped as well). This is a form of financing that allows Series A and B startups to finance capex or other working capital needs even when they are cashflow negative or only at pilot stage from a revenue standpoint. In addition, we are starting to see project finance firms put up the capital for equipment especially if that equipment can be moved or re-used in the event of a default.

However, this form of capital still does not solve for the physical space constraints of creating an industrial food ecosystem. It also does not provide enough capital to truly build large-scale infrastructure and ultimately venture debt is still bound to a startup’s ability to raise its next round. As such it certainly can help a startup as it begins to commercialize but won’t provide the capital required for the industry to mature.

Low-interest government-backed loans

At a cellular agriculture conference last week, alternative protein think tank founder Bruce Friedrich underlined the importance of government support for the cultivated meat sector and he specifically cited low-interest government loans as a key mechanism to boost innovation and help startups scale in a nascent industry, highlighting how vital these loans had been for electric vehicle pioneers.

“Elon Musk says they would have failed twice, if not for long-term low-interest government loans. There is no solar industry, there is no EV [electric vehicle] industry, there is no biopharma industry, if not for governments helping the companies that can’t qualify for standard bank loans, giving them long-term low-interest loans,” said Friedrich. Low-interest government-backed loans have been notably absent as an option for future food founders. One reason for this? Food has not yet reached mainstream consciousness as a key climate concern. This needs to change, given the importance of adapting food systems to reach net global zero goals.

One could argue that no other sector matters as much as food if humanity is to continue to thrive amidst an increasingly acute climate crisis. As such, it’s critical to explore new types of financing and new invested capital formats to support the food tech sector and its community of innovators and entrepreneurs.

Sonalie Figueiras is a journalist, serial climate entrepreneur, longtime food systems change activist and the founding editor of Green Queen Media.

Maximilian von Poelnitz is a venture partner with Ajinomoto helping to set up their new $100m venture capital fund. He has deep experience in food, bio, and climate tech investing following his roles as an investment director and managing partner at DSM Venturing and New Territory Ventures respectively.

Author