European Fermentation Startups Raised More Funds in H1 2024 Than All of 2023

5 Mins Read

Within the first six months of 2024, European precision and biomass fermentation startups attracted more investment than they did in all of 2023.

Between regulatory wins, market breakthroughs, and dominant investment rounds, 2024 has been a seminal year for fermentation-based alternative protein companies.

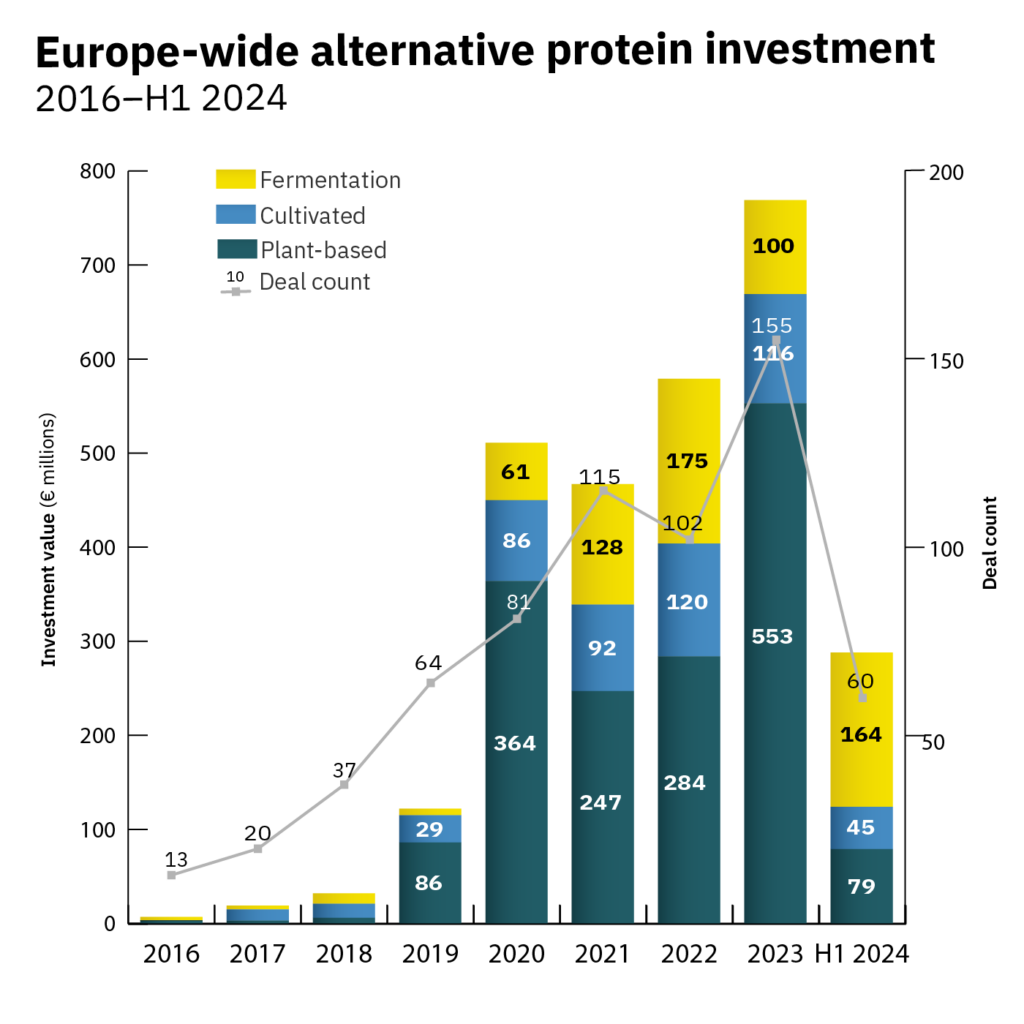

In Europe, precision and biomass fermentation startups have attracted €164M in the first half of this year, surpassing the €100M the sector raised throughout 2023. It means this segment alone has made up 57% of the €287M raised by the alternative protein sector in H1 2024.

Where the industry has suffered is the lack of investment in plant-based proteins and cultivated meat. Companies in the former category have only raised €79M in this period, while those in the latter have secured €45M.

The Net Zero Insights data, published by the Good Food Institute (GFI) Europe, mirrors global trends. While plant-based and cultivated players have lagged, fermentation startups have soared, bringing in $398M in the first six months of 2024 (versus $443M in all of 2023).

Fermentation sector targets scale-up and market entry

Biomass fermentation startups – which use a method similar to beer or yoghurt production to grow large quantities of mycoproteins from fungi – have been the winners so far this year, securing just over €115M by the end of June. This is a 72% rise from last year’s €67M sum.

Meanwhile, companies working with precision fermentation, which involves genetically engineering organisms like yeast to produce bioidentical ingredients like heme, egg and dairy proteins, raised €49 million this year, up from €33M in 2023.

“While it’s great to see investors becoming increasingly confident in this growing sector, it’s also revealing to look at where this money is going,” writes Helene Grosshans, infrastructure investment manager at GFI Europe.

“Many of the fermentation companies that received large investments are focused on leveraging agricultural and food industry sidestreams as a sustainable feed source, helping produce food more efficiently and affordably – both of which are attractive propositions for investors,” she adds.

Grosshans suggests that fermentation startups are using this money to scale up and build the infrastructure necessary to bring their products closer to commercialisation. For example, German startups ProteinDistillery and Infinite Roots, which raised €15M and €53M, respectively, are looking to expand mycoprotein production using raw materials from brewing industries. Finland’s Enifer, meanwhile, brought in €36M to operationalise its mycoprotein factory.

But while the hike in private sector investment is undoubtedly a positive, it isn’t enough for the fermentation sector to overcome one of its biggest bottlenecks: a lack of infrastructure. Some startups are focusing on building pilot plants and factories to aid their commercialisation efforts – but such constriction is expensive.

“Governments should provide grants, loans and guarantees to alternative protein companies to enable infrastructure scale-up and attract additional investments,” says Grosshans.

Contextualising cultivated meat and plant-based investments

Despite the encouraging numbers for fermentation, the investment figures for plant-based and cultivated meat companies leave a lot to be desired.

In 2023, European plant-based startups received €553M in venture capital – but much of this can be attributed to two deals for Oatly, which amounted to €391M. When discounting the oat milk leader’s investment rounds, the gap between 2023 and the first half of 2024 is much smaller.

“This serves as an important reminder that the sector remains immature, with individual company fundraises still capable of having a major impact on the overall figures,” Grosshans writes.

She adds that despite not attracting the massive capital injections seen a few years ago, successful plant-based companies are still bagging large investments, like Spain’s Heura (€40M) and THIS (€25M).

The cultivated meat sector – which has seen three regulatory approvals already this year – is faring slightly better in Europe, having secured 39% of the €116M startups raised in 2023. “Much of this funding is aimed at scaling up the sector – particularly Mosa Meat’s €40M investment aimed at preparing the company for market entry.

Speaking of market entry, France’s Gourmey last month became the first cultivated meat company to officially file a dossier for regulatory approval in the EU, which is expected to be an 18-month-long process.

Public sector funding key for alternative protein

GFI Europe’s analysis comes just weeks after a report by VC firm FoodLabs and investment database Dealroom found that investment in European climate food tech startups overtook the US for the first time in 2023, making up 58% of global funding in the sector and reading €2B.

But globally, food tech investments have suffered, as has the wider VC sector. Alternative protein startups saw funding fall by 44%, but experts are optimistic that the “worst is now behind us”, says Grosshans – although a rebound isn’t expected this year.

An interesting finding of the new European data is that while the number of deals is trending downwards (60 in H1 2024 versus 155 in 2023), the value of these deals is increasing. “Investors are willing to write big cheques but, for now, only to companies with strong metrics,” writes Grosshans.

Government support for innovation sectors is crucial to stimulate private-sector investment. “This particularly applies to alternative proteins, which require significant capital investment to build factories and other scale-up infrastructure, and must compete in the price-competitive food industry,” she says.

A good example is the European Innovation Council (EIC) Accelerator Programme, which has been pouring tens of millions of euros into alternative proteins. Last month, it invested €2.5M each in Dutch palm oil alternative producer NoPalm Ingredients and Swedish precision-fermented fat maker Melt&Marble, as well as €2.4M in oat and mycelium meat maker Millow (also from Sweden). Plus, it was part of Finnish animal-free egg protein maker Onego Bio’s €14M raise in July too.

“In order to realise the climate, economic and societal benefits of alternative proteins, governments need to provide the grants, customised funding solutions and guarantees needed to support the industry, and banks need to provide later-stage capital,” explains Grosshans.

More strategic partnerships with Big Food will help alternative proteins’ case too. These include the collaboration between Leprino Foods – the world’s largest mozzarella manufacturer – and precision fermentation startup Fooditive Group, The Every Company’s animal-free egg partnership with Spain’s Grupo Palacios, and Unilever’s use of Perfect Day’s precision-fermented whey in a new Breyers lactose-free ice cream.

“Private investment has played a central role in enabling the growth of innovative plant-based, cultivated meat and fermentation companies so far,” writes Grosshans. “But new approaches to funding, and collaboration with established food industry players, will be essential for the sector to support Europe’s goals on food security, sustainability and economic growth.”

Author