APAC Agrifood Tech Funding Up by 38%, With India Reclaiming the Top Spot

4 Mins Read

Funding for alternative proteins has grown by 85% this year in Asia-Pacific, mirroring a larger sector-wide recovery, a new AgFunder report shows.

Asia-Pacific’s agrifood tech sector is showing “remarkable” signs of recovery after two years of tumult, with VC investments increasing by 38% so far this year.

By the end of October, companies in the sector had raised $4.2B, reversing a 52% decline from 2023. It has also beefed up APAC’s share in the global agrifood tech funding landscape, which now makes up 31% of the total, up from an average of 26% over the last decade.

The figures come from a new report by AgFunder, in collaboration with Indian VC fund Omnivore and AgriFutures Australia, and signal some respite for businesses working to safeguard the future of food and agriculture.

While investment was still lower than 2020 levels in terms of dollar amounts, the number of deals in the first three quarters of 2024 (616) has already surpassed the full-year totals of each of the last three years, indicating that VCs remain interested in the category, but are more cautious in doling out larger amounts to single companies.

India and China’s dominance complemented by Japan’s jump

The Asia-Pacific AgriFoodTech Investment report found that India has leapfrogged China to the top spot, attracting $2B (or 48%) of the region’s funding this year – although $1B went to a single company, the three-year-old e-grocer Zepto, in two financing rounds.

The world’s most populous country’s agrifood tech industry recuperated significantly from the 73% drop in investments it suffered in 2023. Despite Zepto’s dominant rounds, the number of deals (158) is already 46% higher than the whole of 2023. Green energy specialist Sael’s $299M debt funding ensured that the top three deals belonged to India.

China isn’t too far behind, though, with companies securing $1.5B as of October 2024, 18% higher than this time last year. The country still leads the way in terms of deal count (230), dominating early-stage and Series A rounds. Pig breeding company Shiji Biotechnology Co ($232M) and alcohol producer Serata Moyun ($169M) raised the largest amounts.

The two countries were followed by Japan, which climbed three places to become the surprise success story of the year. Agrifood tech startups in the country brought in $280M (a 58% year-on-year rise) via a total of 93 deals, led by Brewed Protein maker Spiber‘s $65M round. There were signs of this last year, when Japan was the only top 10 APAC nation to see a hike in investments (by 95%).

Australia, however, wasn’t immune to the global downturn, registering a 78% decline in funding year-on-year, with deal count also down by 51%. This has halved its share in the overall APAC market to 1.2% – but in a positive trend, the majority of deals have been closed at the sees stage, indicating renewed activity.

Alternative proteins and novel farm tech rebound

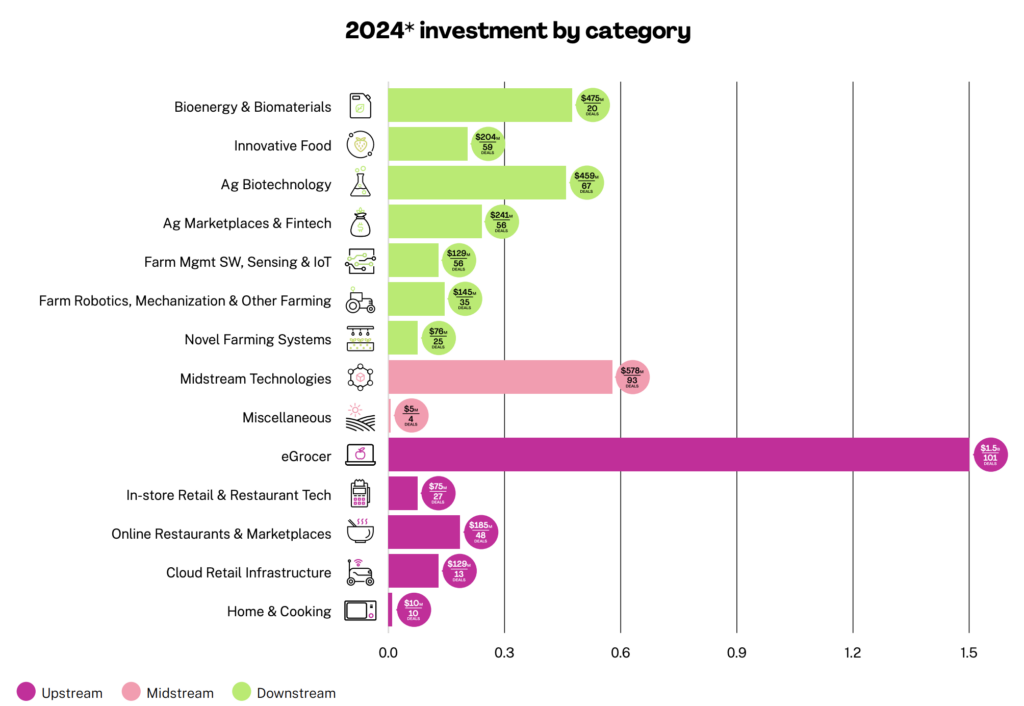

Last year, upstream tech startups (which support farmers and primary production) overtook downstream players (which cover technologies closer to the consumers, like delivery and meal kits) in funding for the first time, but the latter bounced back this year, attracting $1.9B in VC investment.

That said, the gulf between the two has been erased, with upstream companies raising a similar amount ($1.8B) – they also still account for half of the total deal count. Those working with midstream technologies, which connect farmers and food producers to retailers, agro-processors and other clients, secured $525M.

Zepto’s funding success made eGrocery the most well-funded category (raising $1.5B), though deal count also nearly tripled. If you discount Zepto, the upstream categories of Bioenergy & Biomaterials ($475M) and Ag Biotechnology ($459M) were highly attractive to investors this year. The latter’s 30% year-on-year increase was driven by Chinese activity.

Categories labelled Innovative Food (which includes alternative proteins like plant-based foods and cultivated meat) and Novel Farming Systems (covering indoor farms, aquaculture, and insect and algae production) have been the hardest hit on the global stage, but in APAC, they’re rebounding.

Nover Farming Systems posted a small increase from last year with $75M raised over 25 deals. Innovative Food, meanwhile, attracted $204M by the end of October, an 85% increase from the same period in 2023, with deal count also growing from 49 to 59. Singaporean oat milk giant Oatside’s $35M round was the largest in this category.

“APAC is seen as a leader in both of these categories, particularly in Singapore where the government has supported them in search of improved national food security,” the report notes.

In bleaker news, leadership in the agrifood tech sector is still dominated by men, with male-only founding teams making up 92% of the total (from the companies where gender data is available). All-female founders only exist in 3% of businesses, and attract just 0.5% of VC investments (the same as last year). Meanwhile, firms with mixed founding teams saw a dip from 9.3% in 2023 to 8.2% this year.

Author